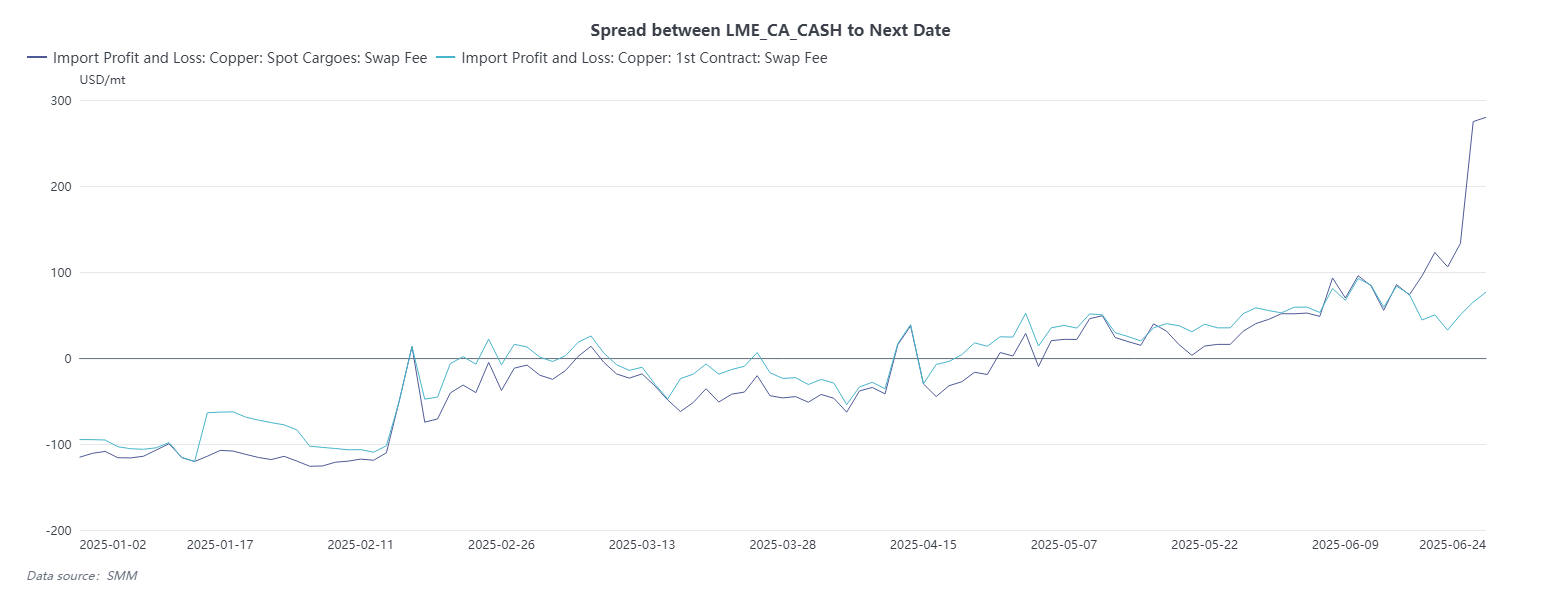

Last Friday evening, the price spread between the LME cash contract and the July date contract suddenly spiked to over $250/mt. As of June 24, the price spread between the two had approached backwardation of $275/mt. This fluctuation sparked various discussions in the imported copper market. Since LME aluminum had experienced similar situation previously, various speculations arose. This article attempts to analyse the recent abnormal structure of LME copper.

Since the LME shifted to a backwardation structure in 2025, the following situations have occurred in the market: before the expiration of the current month contract, the backwardation structure between the current month contract and the next month contract expands. After delivery, the cash contract reverts to a contango structure against the next month contract. The reason lies in the fact that although the LME structure had shifted to backwardation, the inventory level remained relatively high. Additionally, there was Russian copper in Rotterdam warehouses (this type of inventory was considered non-movable), which meant that although some financial positions had expectations for tight supply in the future, supply in the spot market was not tight. This structure provided certain arbitrage opportunities in the market. Taking May as an example, the specific method was: conducting May-June lending before the expiration of the May date contract, converting the May date position into Cash or TOM positions through TOM-NEXT post-delivery, and then establish a Cash-June borrow.

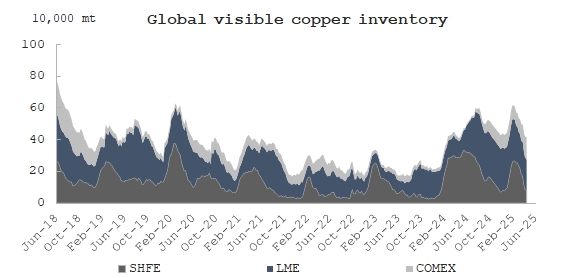

The disappearance of the above-mentioned arbitrage environment can be attributed to the following two reasons: 1. LME inventory has kept falling, reaching around 95,000 mt as of June 24. In particular, the Rotterdam warehouse has experienced significant destocking, with current inventory now below the safety threshold and with a large proportion of cancelled warrants, resulting in extremely low deliverable inventory. 2. The SHFE/LME price ratio has fallen to a point where export window has opened, encouraging Chinese smelters to export more. Given the already high procurement costs of imported copper concentrates, a net short position could easily happen. Therefore, there are sufficient conditions for a significant expansion of the backwardation between Cash-TOM and TOM-NEXT.

In summary, the recent structural anomaly in the LME seems unexpected but is actually a deliberate strategy. The deterioration of copper concentrate treatment charges (TCs) has boosted expectations for tight supply in the future. After the LME structure shifted to backwardation, industrial hedging positions (especially those of smelters) have moved forward significantly. The deterioration of the SHFE/LME price ratio will further raise the procurement costs of copper concentrates, boosting copper cathode exports. As a result, industrial bears have concentrated in the near-month contracts, and a sharp expansion of backwardation is inevitable after inventory falls below the safety threshold.